Opportunity cost is the lost opportunity income from alternative uses of resources.

Analyzing the financial statements of the company, it is impossible to draw any conclusions about opportunity costs. Opportunity costs are those costs that a firm incurs by giving up many other options for using resources in favor of the only one chosen by it.

If resources can be more efficiently used in another project, they should be moved. If such a redistribution of resources does not occur, then the firm loses its possible income. The costs that the firm will incur when reallocating resources between projects should also be taken into account. If they exceed the difference between the yields of alternative projects, then the regrouping of resources between them is not advisable.

For financial management, data on the future cash flows of the enterprise arising from the adoption of a particular management decision are of the greatest interest. In the process of control, the control subsystem must influence the control object. The actual cash flows reflected in the accounting of the enterprise result from previously made management decisions. Information about these flows is an element of feedback between the subject and the control object. It has significant value in substantiating managerial decisions, but the result of these decisions will be to change future, not today's, cash flows. To assess the financial and economic efficiency of the decisions made, it is necessary to compare future cash inflows with future outflows due to the adoption and implementation of these decisions.

For example, in order to make a decision on the release of a new type of product, one should calculate the amount of costs that an enterprise will incur in the production and sale of a new product, and compare this value with the expected income from its sale. At first glance, it may seem quite natural to use for these purposes the calculation of the total cost of 1 product, and by multiplying its amount by the planned sales volume, get the total cost of new products. However, this approach overlooks an important circumstance: a significant part of the total costs is associated with cash flows that took place in the past, even before the decision was made. Implementation of the decision will have no impact on the related cash flows in the future. If it is planned to use the stocks of materials already available at the enterprise for the production of a new product, and their available quantity is sufficient to cover the entire planned need and no new purchases of these materials are foreseen, then the questions arise: what does the cost of purchasing these materials have to do with the release of a new product? Is the refusal of its production will reduce the magnitude of these costs? What real cash outflows will the enterprise incur by using these materials in the process of implementing this solution?

To answer these questions in financial management, the concept is widely used. opportunity cost. In economic theory, opportunity (imputed or economic) costs are understood as the quantity (cost) of other products that should be abandoned or sacrificed in order to get some amount of this product. Returning to our example, it can be argued that the material costs for the production of new products for the enterprise will be equal to the amount that it could earn by selling the stock of materials, since the enterprise has no other alternative to using them. A more general definition of economic costs treats them as the payments that the firm is obliged to make, or the income that the firm is obliged to provide to the supplier of resources in order to divert these resources from use in alternative industries. In our example, the release of a new product will be appropriate for the enterprise if the price that the buyer will offer for it will cover the opportunity costs of both raw materials and materials, and all other resources spent on the production of the product.

The focus of financial management on cash flows generated by management decisions allows us to define opportunity costs as the amount of cash outflow that will occur as a result of making a decision. The decision to launch a new product in production entails a loss of revenue from the sale of materials available at the enterprise. The cost of these materials at the prices of their possible sale will amount to the amount of material costs, which must be taken into account when justifying the corresponding decision.

Distinguish domestic And external alternative costs. If the enterprise did not have stocks of the necessary materials, it would have to purchase them, incurring direct cash costs. In this case, one speaks of external opportunity costs. The enterprise will have to incur the same costs if, for the production of a new product, it needs to hire an additional number of employees of appropriate qualifications. The wages (with all charges on it) of these workers will represent an additional cash outflow, the value of which will characterize the level of external opportunity costs. If you plan to use an internal resource. already available at the enterprise, and paid earlier, regardless of the decision made, then they talk about internal costs. Their value is also determined by the size of future cash outflows, but the nature of these outflows will be different. As a rule, we will not talk about cash costs, but about the loss of additional income. In the case of inventories, this is the price of their possible sale. If, instead of hiring new employees, the enterprise wants to use the labor of existing personnel in the production of a new product, then the value of internal opportunity costs will be determined by the amount of income that the enterprise will lose as a result of distracting employees from their previous occupations. The total opportunity cost of any management decision is equal to the sum of its internal and external opportunity costs

The concept of opportunity costs has become firmly established in scientific circulation. It is used in such training courses as microeconomics, management accounting, as well as in methodological recommendations when determining the opportunity cost of property: "Property invested in a project for the purpose of permanent use, but created before its implementation, is cost".

Opportunity cost theory can help make better policy decisions and provide a clue to forecasting the situation in individual markets. The development of alternative economic thinking of buyers, sellers, managers, politicians is very important in modern economic conditions.

However, despite some attention to the theory of scientists and practitioners, there is a gap between the theory of opportunity costs and the immediate needs of economic decision makers. The author in the article tries to reduce this gap. In particular, two main problems stand out in the application of the theory - the measurement of opportunity costs and alternative valuations in an imperfect market.

1. Choice: freedom and restrictions

An alternative approach is based on the awareness of the fact of limited financial, human, material and other resources, as well as the associated limited freedom of choice. As you know, all benefits are divided into reproducible, non-reproducible and limitedly reproducible. The cost of lost opportunities in relation to reproducible and limitedly reproducible resources (in a more or less long term, sufficient for the emergence of new resources) will be less than in relation to non-reproducible resources. In the case of such a fixed resource as time, its use in one direction means a 100% loss of the possibility of its use in another way.

One of the restrictions on the freedom of an economic entity in choosing alternatives is its budget. We can say that the set of alternatives is dependent on the budget constraint; as this constraint changes, the number of alternatives changes. In addition, for any subject, in any project, one can single out a non-alternative (within its limits, expenses are predetermined, rigidly set) and an alternative (within which it is possible to choose directions for spending funds) parts of the budget. Regardless of what choice a person makes after graduating from a comprehensive school (continuation of education at a university or work), he will spend money on paying for housing, buying food, clothes. This non-alternative part of the costs is not included in the cost of lost opportunities.

The freedom and choice of an economic entity can expand or contract depending on changes in its budget constraint. Thus, softening the budget constraint of an enterprise through a loan, issuing shares allows it to increase the use of material and human resources in some areas (not at the expense of reducing costs in other areas), completely or partially avoiding the costs of lost opportunities.

2. Challenges in measuring opportunity costs

Much has been said about the difficulties of estimating these costs. The author of one of the publications on health economics notes that modern accounting is not aimed at measuring the opportunity costs in medicine, in particular, because of the obstacles to establishing a cost-benefit ratio for each patient.

In some cases, opportunity costs are determined without any problems:

- - when calculating according to the "work-leisure" model. In monetary terms, an alternative estimate of leisure time for working adults is given. This is the hourly rate of pay that they could receive in a paid job;

- - when evaluating various areas of employment. For example, choosing a job as a doctor in a state institution with a monthly salary of UAH 1,500, a specialist loses the opportunity to engage in private practice with a monthly income of UAH 4,000;

- - when assessing internal costs in management accounting. For example, it is possible to evaluate lost wages by the owner of the enterprise and at the same time by its manager; assessment of uncollected rent by the owner of the building, who uses it for his business;

- - when assessing lost opportunities due to keeping money "under the pillow";

- - when comparing different investment projects, when both costs and benefits are expressed in monetary terms. For example, a person decides whether he should invest in his higher education or not. Opportunity costs are defined here in terms of explicit and implicit losses associated with higher education;

- - when calculating and evaluating using indifference curves. Movement along the indifference curve, as is known, shows what alternative price economic agents give to the rejection of one good (the quality of the good) in favor of another good (the quality). In other words, the propensity of an economic entity to sacrifice one good for the benefit of another, the marginal rate of substitution of one good for another, the degree of importance of one good in relation to another are quantified;

- - when assessing using isoquants. The latter show the level of interchangeability of production resources in the production of a certain amount of products.

In some cases, the costs of lost opportunities can be more or less accurately determined only in kind. In the neoclassical concept of the cost of lost opportunities in the field of consumption and demand, the subject sacrifices one utility for the sake of another. The cost of buying and using a certain amount of good A is the impossibility of acquiring and using a certain amount of good B. In other words, the price of good A is expressed in good B. For example, if in order to obtain three units of good A, the subject must sacrifice nine units of good B, then the price of A B will be equal to three.

Speaking about the in-kind measurement of the costs of lost opportunities, it is necessary to pay attention to the following typical example. There are 2 goods: A (guns) and B (oil), and only one factor of production X. This factor can create a unit of good A and 4 units of good B. Therefore, in order to produce a unit of good A, four units of good B must be sacrificed, then is in terms of the alternative price A = 4B, or B = A/4. If prices are equated to opportunity costs, then we get P A P b \u003d 4, where P A is the price of a unit of the good A, a R B - the price of a unit of good B. Thus, the lost opportunities here, too, are reduced to physical terms, to the loss of utility for society. Since utility is difficult to commensurate, the assessment of lost opportunities in this case is also subjective, based on ethical and other non-economic considerations.

In many cases, opportunity costs are not measurable at all or are estimated very roughly due to the need to take into account the huge number of losses and gains as a result of choosing one or another option of behavior. We present some of these cases. Choosing one strategy of functioning and development, the enterprise loses the opportunity to develop in another direction; the country chooses one direction of socio-economic development, while sacrificing another. In both cases, the alternatives available to the enterprise and the state are very difficult to compare due to their heterogeneity and the impossibility of reducing to a common denominator. It is even more difficult to make a cost, monetary assessment of alternatives when it is necessary to take into account the impact of one or another alternative decision on social welfare.

In the practical application of the concept of opportunity cost, an imputation procedure is used. The concept of "imputation", or attribution (imputation), was one of the first to use the Austrian scientists K. Menger and F. Wieser. It means the procedure for linking certain actions of an economic entity with the benefits that it could receive if it took other actions. To implement the imputation procedure, it is necessary to bring costs and benefits to a comparable form. If the benefit is fixed in the form of some goal, then only costs are compared. For example, you can get to work by trolleybus or fixed-route taxi. In this case, when evaluating alternatives, the time and cost of travel to work are compared. In other cases, with cost stability (certain budgetary constraints), benefits and results are compared.

In general theoretical terms, an alternative approach to the analysis of economic processes and phenomena involves the placement of alternatives according to the degree of their attractiveness: efficiency, profitability, quality of results, etc. In practice, the task of assessing economic opportunity costs is to reduce all costs and lost benefits to money and time, then there is something that can be measured. And the imputation procedure without any complications is carried out when the basis for comparison is money or time. For example, to measure the opportunity value of the time of people of working age, the imputation of the time of paid work to leisure is used; or the imputation of the salary that a manager could receive, working for hire, working in his enterprise.

At the same time, imputation procedures will differ with respect to different resources, depending on whether they are currently used or not. It is impossible to impute the time of inactivity of the unemployed person to the salary that he could receive in a paid job.

It should be noted that when comparing alternatives, in some cases, incremental cost-benefit ratios should be used instead of averages (additional costs are compared with additional benefits). In medicine, one type of intervention must be compared not only with other types of intervention, but also with non-intervention.

Difficulties arise when using the imputation procedure. The main obstacle lies in the fact that it is far from always possible to reduce to a common denominator all the losses incurred by the subject when making this or that decision.

It is believed that opportunity costs may be those arising from not using the best of the available opportunities. But what may be lost may not be the optimal, best opportunity, but, say, the so-called second best ( next best), third, etc. Having chosen the optimal option, we lose the opportunities associated with the use of non-optimal options. In each particular case, it is appropriate to ask the question: should the cost of lost opportunities include one unused alternative, some of them, or all of them?

Another problem with assessing lost opportunities is its subjective nature. Subjective in some cases are the ranking of alternatives according to the degree of their attractiveness; the choice of costs and benefits (effects), which are taken into account when comparing various options for economic actions, the use of resources.

The processes concerning alternative estimates, as a rule, affect the interests of different economic actors. An increase in the opportunity price of a resource is beneficial for its sellers and disadvantageous for its buyers. The use of a resource in one direction and non-use in another may meet the interests of one group (person) and not meet the interests of another group (person).

In addition, the decision to choose from several alternatives is in some cases taken by a group of people (in economic policy, in an enterprise). Therefore, the problem arises of assessing the costs of lost opportunities for this group and for each of its members individually. The owner of a large stake in an enterprise can block an alternative that, according to him, entails high opportunity costs for the enterprise as a whole, for all shareholders, but in fact only for him. In the future, the subjective nature of the costs of lost opportunities may become the subject of joint research by representatives of the economic, psychological, and sociological sciences.

Considering the foregoing and recognizing the difficulty of assessing alternative costs, we can propose an algorithm for estimating the opportunity costs of one of the key economic entities - an enterprise: wages, procurement of materials, etc.); 2) promotion of alternatives within the alternative part of the costs; 3) comparison of the discounted flows of "expenses-incomes" for each alternative, placing them according to the level of profitability, the effect obtained, etc.; 4) the implementation of the imputation operation and the assessment of losses when choosing a non-optimal alternative.

For example, the budget for the alternative part of the costs for 5 years is UAH 50 million, which can be spent on the technical re-equipment of one of the workshops, measures to stimulate and retrain employees, advertising and other sales promotion measures. After evaluating the discounted flows of "expenses - incomes" for each direction in a time period of 5 years, it turns out that the technical re-equipment will bring 10 million hryvnias. profits, measures to stimulate and retrain employees - UAH 3 million, and sales promotion measures - UAH 5 million. The imputation of the best alternative - technical re-equipment - to the other two allows us to conclude that the choice of measures to stimulate sales means a loss of 5 million hryvnias, and measures to stimulate and retrain employees - 7 million hryvnias.

3. Alternative valuations in an imperfect market

Market imperfections make alternative valuation of resources difficult. In a perfect market, land, labor and other resources are placed at the disposal of the economic entity that finds the most profitable use for them at the moment and therefore offers the highest price for such a resource. In other words, the value of a resource in a perfect market is indeed determined by its use in the best alternative direction. So, on the market of urban land in Ukraine, which is more or less close to the perfect model, it is no coincidence that this resource has recently been used for the construction of expensive housing and business real estate.

In reality, on the way of a subject capable of ensuring the most efficient use of a resource, there may be various obstacles:

- - erected by the restrictive policy of monopolies, oligopolistic structures, the state;

- -- associated with the lack of information on the availability of such a resource from the most effective potential user;

- -- due to restrictions on the mobility of the resource.

Thus, Employer A can provide the best use and pay a higher salary to a specialist employed by Employer B. However, Employer A is located in another city, employment with him is accompanied by serious moral and psychological costs. Therefore, the specialist remains to work for employer B. Thus, in an imperfect market, the resource can get to a not the most efficient user and receive not the highest (of the possible) rating.

There are the following resource markets: more or less close to the perfect model and imperfect. In addition, there are sectors of the economy where the market does not function at all. At the same time, in the same sector of the economy, both those resources for which the market exists and those for which it does not exist can be used. In medicine, the latter include the time of the patient waiting in line, the time of informal patient care. It should also be noted that in different markets, some one market imperfection stands out "in relief".

It cannot be said that the more perfect the market, the more real the actual prices reflect the opportunity costs, and the actual valuation tends to be more towards the alternative one. It's just that for each good market there is its own alternative price.

Over time, there may be changes in the nature and magnitude of market imperfections. A monopolistic market can become an oligopoly, an oligopoly can approach the model of perfect competition. In place of the state monopoly, a quasi-market can be created. With a change in access to different alternatives, the costs of lost opportunities for economic entities change accordingly. With the reduction of market imperfections, economic agents have new alternatives.

For an effective alternative assessment of a resource, product, service, their market can be created, some imperfections of the market can be eliminated, and reduced. Thus, a quasi-market can be created at the place of state supply of services.

Speaking about the impact of market imperfections on the alternative assessment of a resource, a product, such an assessment should be singled out in different situations: a) during the initial assessment of alternatives for using the resource; b) when there is a problem of diverting already occupied resources from alternative uses. In the second case, the alternative assessment must take into account the costs of overcoming the obstacles associated with the transition from one alternative of using the resource to another. The value of these costs affects the inclusion of one or another alternative in the list of feasible and economically viable alternatives, the value of opportunity costs and price. The magnitude of the cost of transferring a resource from one application to another indicates the degree of market perfection: markets for more flexible, mobile resources are more perfect.

In perfect markets, the establishment of an opportunity price based on opportunity costs occurs automatically, without the participation of external forces. If the market does not function or functions poorly, various institutions are included in the assessment of the resource of the finished product. As a result, it turns out that not the most advanced technologies, samples of goods, services win; vacancies are occupied by not the most deserving workers. In cases where alternative valuation of resources is not possible or complicated, resources are valued at actual prices.

The microeconomic category of opportunity costs can be used in making macroeconomic decisions. The problem of choice at the macro level has long attracted the attention of researchers. Almost all textbooks describe the production possibilities curve. When the economy is at one point on this curve, producing, for example, guns and butter, the opportunity cost of producing more guns is to underproduce a certain amount of butter.

The opportunity costs of decision-making at the macro level are based on the limited resources, primarily the state budget. Let's take as an example such an action as funding unemployment benefits. Having spent money on this action, society to a certain extent is deprived of the opportunity: 1) to subsidize enterprises that could create new jobs that could partially or completely "absorb" the unemployed; 2) provide enterprises with new orders, and therefore - and the opportunity to create additional jobs.

The opportunity cost of investment economic growth in the short term is some restriction of social programs. Intensive budget support for agriculture is accompanied by a lost opportunity to finance the coal industry just as intensively.

It should be noted that the distribution of centralized financial resources across industries, sectors of the economy is associated with the distribution of skilled labor, fuel and energy and other limited resources. Therefore, the redistribution of centralized budgetary funds is always accompanied by the non-receipt of these limited resources by some sectors, sectors of the economy. For example, when making a decision to increase the army from 200,000 to 300,000 people, society loses not only monetary and material resources that could be used for civilian purposes, but also the opportunity to use 100,000 people in a different way. productive population.

It should be noted that the reversibility (irreversibility) of macroeconomic decisions is important for making a decision on the choice of one or another direction of the country's socio-economic development, one or another project financially supported by the state. In the implementation of certain actions, the state, and with it the whole society, bears irreversible costs (sunk costs); that is, it is no longer possible to obtain any additional benefit from the money, material and human resources spent on holding the action.

In other cases, macroeconomic decisions are fully or partially reversible: 1) resources used in development in one direction are then redirected without much difficulty for use in another; 2) the implementation of some public projects is accompanied by positive external effects that are felt by the executors of other state projects.

Choices in macroeconomics are limited. First, each state has social obligations to the population; secondly, there are obligations to support certain sectors of the economy. Without investing a certain minimum in the development of education, health care, and fundamental science, we largely lose them forever, or in the future, significant funds and time may be required to restore them.

Thus, there is a certain non-alternative minimum within which the use of resources cannot be an object of choice, and therefore talking about lost opportunities is inappropriate here.

It should be noted that there is a different degree of urgency in spending funds by the state. Certain areas of spending funds are set strictly (subsidies for housing and communal services, pensions), and under no circumstances can they be an object of choice. Other obligations are not so rigidly fixed, their implementation happens to be neglected. Decisions about the degree of urgency of public spending are largely political.

It should also be taken into account that in macroeconomics the choice is limited by the dependence on the previous development of the country and its institutions. Having taken one step in economic policy, the state in a number of cases partially or completely loses the opportunity to take the second.

In historical terms, the socio-economic development of the country is a chain of successive elections at certain critical time points. The movement of the state from one turning point (node of alternatives) to another is accompanied by a series of lost opportunities. The loss of one of the opportunities at some turning point can be fatal for the country. Getting back to the starting point and making other choices can be costly and time consuming. For Ukraine and other post-Soviet states, we are talking about the fundamental changes in socio-economic life that occurred as a result of the revolutions of 1917, and the subsequent return of countries to the optimal path of development in the 90s of the XX century.

If a course is taken towards a market economy, globalization, a turn in the other direction can be very expensive. Choosing the wrong path for the development of a country, region, industry, state institution entails losses in GNP, output volumes, production effects, social conflicts and upheavals.

But even within the framework of the country's market orientation, its course towards an open economy, the problem of choice and lost opportunities arises. Globalization should be based, in particular, on the relative advantages of the country. It can focus on existing relative advantages (cheap labor, low prices for metal, coal) or change its competitive advantages and enter sectors of the economy where non-price competition prevails.

Opportunity cost is the potential benefit from using capital in a different way than the one that was actually used. Sometimes these costs are also called imputed costs.

In essence, opportunity cost answers the question - how much money would we earn (or how much would we spend) if we acted in a different, alternative way.

The opportunity cost of holding money in cash

Let's take for example that you have 1000 rubles. If you keep this money just at home (“in a jar”), then they will not generate income. Those. in a year you will have the same 1000 rubles.

Another way to store money is a bank deposit. In this case, depending on the type of deposit and the term for which the deposit is opened, the yield will be from 5 to 10%. Take for example - 5% per annum. In this case, in a year you will have 1050 rubles, i.e. 50 rubles more.

The opportunity cost is $50.

The opportunity cost of studying at a university

If a student went to study at a university, then we will assume that he does not work, i.e. does not earn money. Parents pay for his education (i.e., we will consider the opportunity costs of paid education).

If you do not go to study, then:

- first, no need to pay tuition (alternative 1)

- secondly, you can go to work and get paid (alternative 2).

The student loses these two alternatives.

Thus, the opportunity cost of acquiring higher education is equal to the cost of education + earnings for 5 years of work (which was not received).

At the same time, it is important to understand that the opportunity costs of paid education do not include, for example, the cost of buying food or clothes, since you will need to eat and dress in any of the options - both during training and if you do not study.

The opportunity cost of building a new stadium

When building a new stadium, alternative capital investment options would be, for example:

- construction of schools, kindergartens

- construction of houses in this area

- or construction of a shopping mall or office building

It turns out that the opportunity cost of the stadium will be the difference in price between these objects and the new stadium, which is obviously one of the most expensive objects to build.

Topic: Opportunity cost concept

Type: Test | Size: 27.03K | Downloads: 29 | Added on 02/23/10 at 11:30 | Rating: +2 | More Examinations

University: VZFEI

Year and city: October 2009

Introduction 3

Chapter 1. The concept and types of production costs 4

1.1. Fixed and variable costs 4

1.2. Opportunity cost 6

Chapter 2 Opportunity Cost Concepts 8

2.1. Cost calculation 8

2.2. Applications of the cost concept 17

Chapter 3. Applying the Opportunity Cost Concept 19

Conclusion 21

Tasks 23

Test items 24

References 26

Introduction

The concept of opportunity cost at first glance may seem like a rather exotic abstraction that cannot be used in practical financial activities. Indeed, why engage in abstract logical constructions, when almost every enterprise has accounting data on the full actual costs of acquiring any asset? There are even frequent disputes about which method of determining costs is more objective: “accounting” or the method of calculating opportunity costs. The very formulation of such a question does not seem quite correct. The main difference between these methods is not in "accuracy" and "objectivity", but in their purpose. When analyzing the financial statements of an enterprise, any researcher without a shadow of a doubt uses accounting data to calculate the liquidity ratio or the availability of own working capital. Exactly the same interest is presented by the indicators of financial statements for tax inspectors, auditors, auditors who check the activities of the enterprise. Common to all these categories of users of reporting information is the desire to understand the transactions that have already been completed.

The relevance of the topic chosen for the study lies in the importance of applying the concept of opportunity costs.

The purpose of the control work is to study the planning and cost accounting, which become important in management decisions. To achieve this goal, the following tasks are solved:

- Analyze the types of costs;

- Consider the concept of opportunity cost;

- To study the application of the concept of opportunity cost.

The subject of the study is the calculation of opportunity costs, forms of manifestation of the concept of opportunity costs.

Chapter 1. The concept and types of production costs

1.1. Fixed and variable costs

Speaking about production costs, K. Marx considered the process of formation of costs directly according to their main elements in the production process. He abstracted from the problem of price fluctuation around value. In addition, in the twentieth century, it became necessary to determine the changes in costs depending on the amount of output produced.

Modern concepts of costs largely take into account both of the above points. In the center of the classification of costs is the relationship between the volume of production and costs, the price of a given type of goods. Costs are divided into independent and dependent on the volume of production.

Fixed costs do not depend on the size of production, they exist even at zero volume of production. These are the previous obligations of the enterprise (interest on loans, etc.), taxes, depreciation, payment for security, rent, equipment maintenance costs at zero production volume, salaries of management personnel, etc. Variable costs depend on the quantity of products produced, they consist of the costs of raw materials, materials, wages to workers, etc. The sum of fixed and variable costs forms gross costs - the amount of cash costs for the production of a certain type of product. To measure the cost of producing a unit of output, the categories of average, average fixed and average variable costs are used. The average cost is equal to the quotient of dividing the total cost by the quantity of output produced. Average fixed costs are determined by dividing the fixed costs by the quantity of output produced. Average variable costs are formed by dividing the variable costs by the amount of output produced.

To achieve maximum profit, you need to determine the required amount of output. The tool of economic analysis is the category of marginal costs. Marginal cost is the incremental cost of producing each additional unit of output over a given level of output. They are calculated by subtracting adjacent gross costs.

1.2. opportunity cost

In real production activities, it is necessary to take into account not only the actual cash costs, but also the opportunity costs. The latter arise because of the possibility of choosing between certain economic solutions. For example, the owner of an enterprise can spend the available money in various ways: he can use it to expand production or spend it on personal consumption, etc. Measurement of opportunity costs is necessary not only for market relations, but also for objects that are not goods. In an unregulated market for goods, the opportunity cost will be equal to the current, currently established market price. If there are several different (usually close) prices on the market, then the opportunity cost of selling the product at, naturally, the highest price offered to the seller by buyers will be equal to the highest of all remaining (except the highest) prices offered.

Earlier in the USSR, the construction of hydroelectric power stations (HPPs) on rivers flowing through the plains was widespread. It is possible to receive income from the production of electricity during the construction of a dam, the creation of a reservoir and the installation of a hydroelectric power station. If this construction is abandoned, it is possible, with the help of the released monetary and material resources, to receive income from intensive coastal agriculture, fishing, forestry and other economic activities on lands that can be turned into the bottom of the hydroelectric reservoir. The total economic costs of obtaining electricity will be equal to the sum of the costs of building a hydroelectric power station and the valuation of the possible volume of production from intensive economic activity on flooded lands (opportunity costs). The total economic costs of any kind of economic activity should include, in addition to the usual monetary and material, also opportunity costs, covering the valuation of the best possible alternative decision on the use of available resources (labor, money, material, etc.).

Chapter 2 Opportunity Cost Concepts

2.1. Cost calculation

Production costs are expenses, cash expenditures that must be made to create a product. For an enterprise (firm), they act as payment for the acquired factors of production.

Such expenses cover payment for materials (raw materials, fuel, electricity), wages of employees, depreciation, costs associated with production management. When selling goods, the entrepreneur receives cash proceeds. One part of it compensates for the costs of production (i.e., the cost of money associated with the production of goods), the other gives a profit, that for which production is organized. This means that the cost of production is less than the cost of goods by the amount of profit

Simplifying the concept, we can say that the costs of the enterprise are understood as what it costs to produce products.

For financial management, data on the future cash flows of the enterprise arising from the adoption of a particular management decision are of the greatest interest. In the process of control, the control subsystem must influence the control object. The actual cash flows reflected in the accounting of the enterprise result from previously made management decisions. Information about these flows is an element of feedback between the subject and the control object. It has significant value in substantiating managerial decisions, but the result of these decisions will be to change future, not today's, cash flows. To assess the financial and economic efficiency of the decisions made, it is necessary to compare future cash inflows with future outflows due to the adoption and implementation of these decisions.

For example, in order to make a decision on the release of a new type of product, one should calculate the amount of costs that an enterprise will incur in the production and sale of a new product, and compare this value with the expected income from its sale. At first glance, it may seem quite natural to use for these purposes the calculation of the full cost of one product, and, multiplying its amount by the planned sales volume, get the total cost of new products. However, this approach overlooks an important circumstance: a significant part of the total costs is associated with cash flows that took place in the past, even before the decision was made. Implementation of the decision will have no impact on the related cash flows in the future. If it is planned to use the stocks of materials already available at the enterprise for the production of a new product, and their available quantity is sufficient to cover the entire planned need and no new purchases of these materials are foreseen, then it is not known how the costs of purchasing these materials are related to the release of a new product and what real cash outflows will be incurred by the enterprise, using these materials in the process of implementing this decision.

In connection with these unknown quantities, the concept of opportunity costs is widely used in financial management.

In economic theory, opportunity (imputed or economic) costs are understood as the quantity (cost) of other products that should be abandoned or sacrificed in order to get some amount of this product. It can be argued that the material costs for the production of new products for the enterprise will be equal to the amount that it could earn by selling the stock of materials, since the enterprise has no other alternative to using them.

A more general definition of economic cost is the payment that a firm is required to make, or the income that a firm is required to provide, to a supplier of resources in order to divert those resources away from use in alternative industries. The release of a new product will be appropriate for the enterprise if the price offered by the buyer for it will cover the opportunity costs of both raw materials and materials, and all other resources spent on the production of the product.

The focus of financial management on cash flows generated by management decisions allows us to define opportunity costs as the amount of cash outflow that will occur as a result of making a decision. The decision to launch a new product in production entails a loss of revenue from the sale of materials available at the enterprise. The cost of these materials at the prices of their possible sale will be the amount of material costs, which should be taken into account when justifying the corresponding decision.

Distinguish between internal and external opportunity costs. If the enterprise did not have stocks of the necessary materials, it would have to purchase them, incurring direct cash costs. In this case, one speaks of external opportunity costs. The enterprise will have to incur the same costs if, for the production of a new product, it needs to hire an additional number of employees of appropriate qualifications. The wages (with all charges on it) of these workers will represent an additional cash outflow, the value of which will characterize the level of external opportunity costs.

If it is planned to use an internal resource that is already available at the enterprise and paid for earlier, regardless of the decision made, then they talk about internal costs. Their value is also determined by the size of future cash outflows, but the nature of these outflows will be different. As a rule, we will not talk about cash costs, but about the loss of additional income. In the case of inventories, this is the price of their possible sale. If, instead of hiring new employees, the enterprise wants to use the labor of existing personnel in the production of a new product, then the value of internal opportunity costs will be determined by the amount of income that the enterprise will lose as a result of distracting employees from their previous occupations.

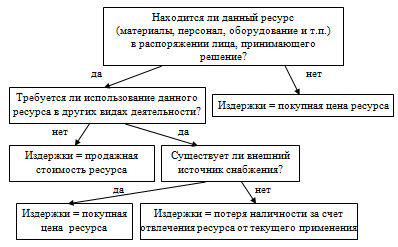

The total opportunity cost of any management decision is equal to the sum of its internal and external opportunity costs. Better assimilation of the concept of opportunity costs is facilitated by the use of the flowchart proposed by the English scientist B. Ryan:

Figure - Decision-making algorithm for opportunity costs

Let us consider an example of using this reasoning scheme in the course of estimating the value of opportunity costs. The enterprise received an order for the sale of a batch of products in the amount of 5000 pieces at a price (without VAT) of 40 rubles per 1 piece. This product has been mastered by the enterprise, but recently its production has not been carried out due to lack of demand. For its manufacture, a single type of material is required, the stock of which in the amount of 2.5 tons is available at the enterprise and must be renewed in the same volume. The purchase price of the material at the time of the last purchase was 30 rubles. per 1 kg (excluding VAT), but currently it has increased by 5%. For the production of 1 product, 0.5 kg of this material is required. The labor intensity of 1 product is 0.4 standard hours, the hourly tariff rate of the main workers employed in its production (including social charges) is 25 rubles. To complete the order within 10 days, it is necessary to attract 25 workers for this period, of which 10 will be re-hired under a labor agreement for 10 days, 10 will be used from among full-time employees temporarily idle due to lack of work, 5 will be distracted from others works. Labor productivity and wages for each of the 25 workers will be the same. General production costs of the enterprise are 100% of the basic wages of the main production workers; general business expenses - 50% of the same base. Non-manufacturing (commercial) expenses amount to 5% of the production cost of products sold.

Having such data, the planning department of the enterprise compiled the following calculation of the total planned cost of products (Table 1).

Planned calculation of the full cost of 1 product, rub.

Table 1.

|

Expenditures |

||

|

1. Main materials |

||

|

2. Basic salary (with accruals) |

||

|

3. General production costs |

||

|

4. General expenses |

||

|

Production cost of 1 product |

||

|

5. Non-production (commercial) expenses |

||

|

Full cost of 1 product |

It follows from the calculation that on each product the enterprise will lose 2 rubles (42 - 40), which, based on the entire output, will be 10 thousand rubles. (2 x 5000) loss. It is obvious that the enterprise should not agree to the execution of an order that brings him losses. However, by calculating the opportunity costs for this order, you can get a different result. First of all, it is necessary to study additional initial data: during the downtime, the enterprise accrues wages at the rate of 30 rubles per employee. in a day. 5 people who are planned to be diverted from their work receive 125 rubles each. in a day. Transferring them to another job for 10 days will mean a loss of income for the enterprise in the amount of 35 thousand rubles, due to a decrease in the output of their products. In connection with the implementation of a new order, not all indirect costs of the enterprise will increase, but only their variable part, which is calculated at the following rates: production overhead costs - 10 rubles. for each additional standard hour of the scope of work; variable selling expenses - 2 rubles, for each additional product sold.

Given these conditions, the calculation of opportunity costs will have the following form:

1. Calculation of material costs. At the time of the decision, the enterprise had the necessary amount of materials that it did not intend to use for another purpose. The decision to fulfill the order could not affect their cost, so the actual costs of purchasing already existing materials should not be taken into account. The company plans to renew this stock at a higher price of 31.5 rubles. per 1 kg (30 + 0.05 x 30), therefore, the opportunity costs for the purchase of the same amount of materials will amount to 78.75 thousand rubles. (31.5 x 2500). These costs are associated with the internal reallocation of resources, they do not follow directly from the decision to release new products, since the materials were already in the warehouse of the enterprise, so they should be attributed to internal opportunity costs.

2. Calculation of the cost of wages. The wages of 10 newly recruited temporary workers are fully conditioned by this decision. Based on an 8-hour working day, the amount of payment for their work for 10 days of work will be 20 thousand rubles. (10 people x 8 hours x 10 days x 25 rubles). Unloaded full-time workers currently receive time wages at the rate of 30 rubles. in a day. Therefore, the opportunity cost of their wages will amount to 17 thousand rubles. (10 people x 8 hours x 10 days x 25 rubles - 10 people x 10 days x 30 rubles). The distraction of another 5 full-time employees from the work performed will entail a loss of income of the enterprise by 35 thousand rubles, this amount should be taken into account as part of opportunity costs. At their previous job, their salary was 125 rubles. per day, therefore, the total cost of their wages will be 38,750 rubles. (5 people x 8 hours x 10 days x 25 rubles - 5 people x 10 days x 125 rubles + 35,000 rubles). In total, the enterprise's opportunity costs for wages will be equal to 75,750 rubles. Of these, additional cash outflows due to the decision under consideration (external costs) will amount to 50 thousand rubles. (25 people x 8 hours x 10 days x 25 rubles); losses associated with the diversion of resources (internal costs) will amount to 25,750 rubles. (35,000 rubles - 10 people x 10 days x 30 rubles - 5 people x 10 days x 125 rubles).

3. Calculation of overhead and commercial expenses. The labor intensity of the additional production of 5000 products will be 2000 standard hours (5000 x 0.4). Therefore, the increase in variable overhead production costs will be equal to 20 thousand rubles. (2000 x 10). The increase in variable commercial expenses will be 10 thousand rubles. (5000 x 2). These costs are decision-driven, so they are external opportunity costs. Fixed indirect costs will remain unchanged in any case, so they should not be included in the opportunity cost calculation for this decision.

Summarizing the performed calculations, we construct Table 2.

Calculation of opportunity costs, thousand rubles

table 2

|

Expense items |

opportunity cost |

||

|

domestic |

|||

|

1. Direct materials |

|||

|

3. Variable manufacturing overheads |

|||

|

4. Variable selling expenses |

|||

|

Total opportunity cost |

|||

Thus, the total opportunity costs will amount to 184.5 thousand rubles, which is 15.5 thousand rubles lower than the cost of selling 5000 products (200 thousand rubles). It turns out that it is beneficial for the enterprise to agree to the execution of the order, since the proceeds received will not only cover all the costs associated with it, but will also provide a contribution to cover its fixed costs in the amount of 15.5 thousand rubles.

However, the amount of fixed costs of the entire enterprise is much higher than 15.5 thousand rubles. And therefore, when planning its activities, an enterprise must form such a portfolio of orders so that their totality covers all fixed costs and ensures profit. If this cannot be achieved, then it is necessary to reduce fixed costs that are not directly related to the production and commercial activities of the enterprise. It does not have the luxury of investing its financial resources in capacity development that does not bring real returns. In any case, we are talking about qualitatively different decisions that have nothing to do with the decision to fulfill a specific order. If the company has a choice, then, of course, one should prefer a more profitable option that provides maximum coverage of fixed costs. But the lack of choice cannot be a reason for not producing products whose price is higher than their opportunity cost.

By refusing to produce products that fully cover their opportunity costs in the hope of obtaining better orders that pay for the full cost of each product, the company loses real cash inflows from hands, chasing expected higher cash inflows in the future. Such behavior is contraindicated both for a financial manager and for any businessman. Business owners (investors) pay their managers the only service - the real increase in invested capital. A manager should not turn down the opportunity to secure at least a minimal capital increase if he does not have a real alternative opportunity for a more profitable use of the assets.

2.2. Forms of application of the concept of costs

The following forms of practical manifestation of the considered concept of opportunity costs can be distinguished:

1. When justifying financial decisions, one should focus primarily on the cash flows generated by these decisions. Here it is appropriate to recall again the expression of B. Ryan, modestly defined by him as "Ryan's Second Law": "Costs and incomes arise only at those moments when cash flows cross the boundaries of the enterprise." Without questioning the value and importance of calculating the full cost, financial management operates with slightly different concepts, the central one among which is cash flow.

2. Those and only those cash flows that are directly related to this decision should be taken into account. Receipts and expenditures of funds, regardless of the time of their occurrence, not related to the decision being made, should not be taken into account. In other words, financial management works with incremental cash flows, and the opportunity costs considered in it are marginal. If, as a result of a decision to release a new product, it is necessary to hire additional security guards to the staff of the enterprise, then the marginal costs of maintaining new security workers should be included in the cost of the product being mastered, while the costs of maintaining security guards in the previous amounts are not relevant to this decision and in opportunity costs should not be included.

3. The decision taken cannot affect the expenses already incurred or the income received earlier. Therefore, justifying this decision, the financial manager should take into account only future cash flows. All past payments and receipts, including the cost of purchasing equipment, are of a historical nature, they can no longer be avoided or prevented. Therefore, such an element of costs as depreciation of fixed assets does not participate in financial calculations.

Chapter 3. Applying the Opportunity Cost Concept

The application of the concept of opportunity costs poses serious challenges for the information subsystem of financial management. It is obvious that the data of traditional accounting alone is not enough in this case. There is a need to create an accounting system focused on a more complete and accurate identification of opportunity costs - a management accounting system. The cornerstone of such a system is the division of all expenses of the enterprise into conditionally fixed and variable parts in relation to the volume of output (sales) of products.

Planning and accounting for costs in this context makes it possible to more closely link them with the consequences of specific management decisions, to exclude the possibility of “overlapping” the financial results of this decision with the influence of factors unrelated to it (for example, general factory overhead costs).

Another distinguishing feature of such systems is the wide coverage of enterprise costs by rationing. This allows you to more accurately predict future cash inflows and outflows.

The third feature of management accounting systems is the personification of information, the linking of accounting objects with the areas of responsibility of specific managers, which makes it possible to even more clearly delimit the costs that depend on specific decisions from all other costs that are not related to it.

The listed features are reflected in such accounting systems as the standard method of accounting for production costs (standard-cost system), accounting for variable costs (direct costing), accounting for cost centers, profit centers and responsibility centers.

At Russian enterprises, all these systems take root rather slowly, despite the fact that the introduction of the standard method of cost accounting, for example, has been going on for over 60 years. It seems that one of the reasons for this situation is the underestimation by the management of enterprises of the managerial and financial functions of these methods. It is still believed that they are just varieties of general accounting and the solution of emerging issues is at the mercy of the accounting personnel of enterprises. But accounting workers face a completely different task - the timely and reliable determination of the total cost of historical costs, for which traditional calculation methods are quite sufficient.

For ordinary accounting, the division of costs into variable and fixed parts is much less important than dividing them into direct and indirect costs. Solving fundamentally different tasks in comparison with financial management, the accountant perceives the task assigned to him in a different way. For him, the new method of accounting is, first of all, a different way of allocating indirect costs between products (or refusing to do so in the case of the direct costing method). And since the introduction of any new method is associated with additional costs, not seeing a significant benefit from such a replacement, the counting worker subconsciously opposes changes that can bring him nothing but additional inconvenience and unnecessary work.

Thus, being one of the main consumers of general (financial) accounting information, financial management is also interested in creating a management accounting system focused on controlling alternative costs. According to a number of properties, this system should differ significantly from traditional accounting, therefore, when creating it, the requirements and needs, first of all, of financial management should be taken into account. It is quite possible that even the organizational status of the relevant unit may differ from the status of general accounting and its operational activities, the financial director, rather than the chief accountant of the enterprise, will have a greater influence.

Conclusion

Each production unit (enterprise) of any society seeks to obtain the greatest possible income from its activities. Any enterprise tries not only to sell its goods at a profitable high price, but also to reduce its costs for production and sale of products. If the first source of increasing the income of the enterprise largely depends on the external conditions of the enterprise, then the second - almost exclusively on the enterprise itself, more precisely, on the degree of efficiency of the organization of the production process and the subsequent sale of manufactured goods.

Many economists have made significant contributions to the study of costs. Production costs are understood as the costs of wages, raw materials and materials, this also includes depreciation of labor instruments, etc. Production costs are the costs of production that the organizers of the enterprise must incur in order to create goods and then make a profit. In the cost of a unit of goods, the cost of production is one of its two parts. Production costs are less than the cost of goods by the amount of profit.

The financial manager is faced with the task of designing a future financial transaction, assessing as accurately as possible all the possible benefits and losses associated with this particular operation. At the same time, he in no way rejects the already available “historical” data, on the contrary, the analysis of financial statements is one of the most important tasks of financial management. However, in order to justify financial decisions aimed at obtaining future results, appropriate tools with specific properties are needed. The concept of opportunity costs forms the theoretical basis of such tools, therefore it is often not presented in an explicit form, and many practitioners, performing financial calculations, use this concept without even knowing about its existence.

Tasks

Task 1

The enterprise's profit before interest and taxes amounted to 4 million rubles, the amount of interest on the loan was 1.5 million rubles, the income tax rate was 20%. Evaluate the effectiveness of the organization's borrowing policy based on the following balance sheet data:

|

Asset, million rubles |

Liabilities, million rubles |

||

|

Buildings and constructions |

Equity |

||

|

Borrowed capital, including: Short long term |

|||

|

Inventory |

|||

|

Accounts receivable |

|||

|

Cash |

|||

ER = (4.0: 14) * 100% = 28.6%

SRSP \u003d (1.5: 6) * 100% \u003d 25%

EDR \u003d (1 - 0.2) (28.6 - 25) \u003d 6 \\ 8 \u003d 2.16%

Task 2

The depositor placed 40 thousand rubles in the bank for 4 years. Simple interest is charged: in the first year - at a discount rate of 8%, in the second - 7%, in the third - 9%, in the fourth - 7%. Determine the future value of the investment by the end of the fourth year.

S \u003d 40000 (1 + 0.08 + 0.07 + 0.09 + +0.07) \u003d 52.4 thousand rubles.

Test tasks

1. The level of risk of loss of profit is greater if:

1. natural volume of sales decreases and prices rise at the same time

2. natural volume of sales is growing and at the same time prices are falling

3. Prices and volume of sales decrease

Rationale:

Demand for products falls, and price increases reduce demand even more. and all this reduces the volume of sales.

According to the mechanism of operating leverage, any decrease in the volume of sales of products will further reduce the size of gross operating profit.

2. Bank deposit for the same period increases more when interest is applied

1. simple

2. complex

Rationale:

A deposit in the amount of 50 thousand rubles was accepted. for a period of 90 days at a rate of 10.5 percent per annum. Calculate the amount of a bank deposit using simple and compound interest.

Simple interest:

Sp \u003d 50000 x 10.5 x 90 / 365 / 100 \u003d 1294.52

S = 50000 + 1294.52 = 51294.52

Compound interest (with interest compounded every 30 days)

S \u003d 50000 x (1 + 10.5 x 30 / 365 / 100) 3 \u003d 51305.72

Sp \u003d 50000 x [(1 + 10.5 x 30 / 365 / 100) 3 - 1) \u003d 1305.72

As a result, for 90 days, compound interest amounted to 11.2 rubles. more.

3. Operating leverage evaluates:

1. cost of products sold

2. sales proceeds

3. degree of profitability of sales

4. a measure of profit sensitivity to changes in prices and sales volumes

Rationale.

Operating leverage, by definition, shows how many times operating profit changes with an increase in revenue.

4. The elements of risk classification according to the level of financial losses are:

1. acceptable risk

2. external risk

3. tax risk

4. simple risk

Rationale:

According to the level of financial losses, the risk is divided into: acceptable, critical, catastrophic.

External risk is a classification according to the sphere of occurrence.

Tax risk is a classification by types of financial risks.

Simple risk is a classification according to the possibility of further classification.

5. Enterprises No. 1 and No. 2 have equal variable costs and equal profit from the sale, but the sales revenue in enterprise No. 1 is higher than in enterprise No. 2. The critical volume of sales will be greater in the enterprise:

1. № 1

Rationale.

The critical sales volume can be defined as the sales volume at which marginal profit equals fixed costs. Enterprise No. 1 has higher sales revenue, therefore, the critical sales volume is also higher (ceteris paribus).

List of used literature

- Kovalev V.V. Introduction to financial management. - M.: Finance and statistics, 2007. - 768 p.

Friends! You have a unique opportunity to help students like you! If our site helped you find the right job, then you certainly understand how the work you added can make the work of others easier.

If the Control Work, in your opinion, is of poor quality, or you have already met this work, please let us know.

- Opportunity costs, costs of lost profits or costs of alternative opportunities (eng. Opportunity cost) - an economic term denoting lost profits (in a particular case - profit, income) as a result of choosing one of the alternative options for using resources and, thereby, rejecting other opportunities . The amount of lost profit is determined by the utility of the most valuable of the discarded alternatives. Opportunity costs are an inseparable part of any decision making. The term was introduced by the Austrian economist Friedrich von Wieser in his monograph The Theory of Social Economy in 1914.

Opportunity costs can be expressed both in kind (in goods, the production or consumption of which had to be abandoned), and in the monetary equivalent of these alternatives. Also, opportunity costs can be expressed in hours of time (lost time in terms of its alternative use).

The theory of opportunity cost is described in the monograph "The Theory of the Social Economy" in 1914. According to her:

productive goods represent the future. Their value depends on the value of the final product;

the limited resources determine the competitiveness and alternative ways of their use;

production costs are subjective and depend on the alternative possibilities that have to be sacrificed in the production of a certain good;

the real value (utility) of any thing is the lost utility of other things that could be produced using the resources spent on the production of this thing. This provision is also known as Wieser's Law;

imputation is carried out on the basis of opportunity costs - the costs of lost opportunities. The contribution of von Wieser's theory of opportunity costs to economics is that it is the first description of the principles of efficient production.

Opportunity costs are not expenses in the accounting sense; they are just an economic construct to account for lost alternatives.

Related concepts

Smith's dogma is one of the fundamental theses of classical political economy, formulated by Adam Smith, according to which the price (exchange value) of the annual product of a society is calculated as the sum of the incomes of all members of society. "Smith's dogma" is studied in the program of the modern course of the history of economic doctrines, along with other provisions of classical political economy.

The costing argument is one type of criticism of the planned economy. It was first proposed by Ludwig von Mises in 1920 and later studied in detail by Friedrich Hayek.

Profit is the positive difference between total income (which includes proceeds from the sale of goods and services, received fines and compensation, interest income, etc.) and the costs of production or acquisition, storage, transportation, and marketing of these goods and services. Profit \u003d Revenue - Costs (in monetary terms).

References in literature

The economic cost is opportunity cost enterprises. They include accounting (explicit) and implicit (internal) costs, which are the property of the enterprise, for which it does not pay. Therefore, internal costs include income on own resources within a nominal percentage, that is, if they were rented out, and normal profit, determined by the wages and remuneration of the entrepreneur, as if he were employed. Economic costs are used to decide whether to continue the adopted business policy or change it.

The counterargument to the benefits of diversification is based on the assumption that diverging asset classes can lead to significant opportunity cost. Naturally, this argument relies on knowledge of past results. Diversification is about the future and its uncertainty, which we cannot predict. This is a counterargument we hear all the time from serious gold bugs (investors who deal exclusively in gold). We, in turn, could look at the lost opportunities they suffered in 2010 due to investments in gold, which returned a measly 30%, while silver rose by 70%. If you recalculate the price of gold in terms of the price of silver, it has lost 23% of its value. A similar argument can be made for the benefits of investing in residential real estate, which has outperformed gold over the past 15 years, despite falls in 2007 and 2008. These are, of course, extremes, but we think they only emphasize that investing everything in gold is just as unwise as giving it up completely.

In the absence of clear and detailed information about new financial instruments, their use can be at least useless for business. In odious cases, unmanaged supply in the technology market can harm consumers by provoking abuse by better-informed market participants. The legal and informational vacuum thus becomes a risk factor. The guiding criterion for mastering innovations is opportunity cost determined by the ratio of industrial applicability/novelty of the technology and the costs of its implementation, including due to the lack of legal certainty.

Under opportunity cost are understood as those that must be introduced when assessing the future situation, when there is an alternative for making various decisions. The use of opportunity costs is justified in the analysis based on insufficient (scarce) resources. When analyzing the situation on the basis of excess resources, the opportunity cost is zero.

The production possibilities curve has several levels, each of which is represented by a new kind of combination of goods in their monetary terms. Through technological innovations, the development of scientific and technical progress products, the discovery of qualitatively different ways of extracting natural resources, progress in the economy is quite real, which is marked by a transition to a new, higher level of the transformation curve. In this connection, the concept opportunity cost: these are non-produced goods, i.e. those that were discarded as a specialization option at an early stage of production.

This inverse relationship is also increasing: the minimum price for producing and selling more of the same product always increases, mainly due to the increase in opportunity cost. The relationship between the direct and inverse functions of the proposal can similarly be considered using the example of linear dependence.

1) explicit (external). Explicit costs are the firm's payments to suppliers of inputs and intermediate products. They are paid in cash when the factors of production are not owned by the firm. Explicit costs include: wages paid to workers; managers' salaries; commission payments to trading firms; payments to banks and other financial service providers; fees for legal advice, travel expenses and more. Explicit costs do not exhaust all types opportunity cost, which is carried by the firm in the production process;

However, as a financial asset, money only retains value (and even then only in a non-inflationary economy), but does not increase it. Cash has absolute (100%) liquidity, but zero yield. At the same time, there are other types of financial assets, such as bonds, which generate income in the form of interest. Therefore, the higher the interest rate, the more a person loses by holding cash and not buying interest-bearing bonds. Consequently, the determining factor in the demand for money as a financial asset is the interest rate. At the same time, the interest rate is opportunity cost storage of cash. A high interest rate means high bond yields and high holding costs, which reduces the demand for cash. With a low rate, i.e., low costs of holding cash, the demand for it increases, because with a low return on other financial assets, people tend to have more cash, preferring its property of absolute liquidity. Thus, the demand for money depends negatively on the rate of interest. The negative relationship between the speculative demand for money and the interest rate can be explained in another way - from the point of view of people's behavior in the securities (bonds) market.

Related concepts (continued)

Transaction costs (eng. transaction cost) - costs arising in connection with the conclusion of contracts (including using market mechanisms); costs accompanying the relationship of economic agents.

New Keynesianism is a school of thought in modern macroeconomics, which is a development of the ideas of John Maynard Keynes. "New Keynesianism" redefined the role of monetary policy and the mechanical separation of microeconomics and macroeconomics in neo-Keynesianism.

Deviation towards the status quo is one of the cognitive distortions, expressed in the tendency of people to want things to remain approximately the same, that is, to maintain the status quo. The effect arises from the fact that the damage from the loss of the status quo is perceived as greater than the potential benefit of changing it to an alternative option.

The Lucas aggregate supply function describes aggregate supply according to the Lucas imperfect information model and is based on the research of the neoclassical economist Robert Lucas. According to the model, output in the economy is a function of "money surprise" or "surprise prices" (English "money" or "price surprise"), that is, not consistent with rational expectations. In this case, the actual price turns out to be higher than expected, which leads to a short-term excess of the actual...

The Lausanne school of marginalism is one of the scientific schools of the neoclassical direction in the economic theory of the late 19th - early 20th centuries. The main representatives are Leon Walras (1834-1910) and Vilfredo Pareto (1848-1923).

A free market is a market free from any outside interference (including government regulation). At the same time, the function of the state in the free market is reduced to the protection of property rights and the maintenance of contractual obligations. Also, a free market is defined as a market where prices are set freely without outside interference and other external factors, solely on the basis of supply and demand. The basis of a free market is the right of any manufacturer to create ...

Macroeconomics (from other Greek μακρός - "long", "big", οἶκος - "house" and Nόμος - "law") - a section of economic theory that studies the functioning of the economy as a whole, the economic system as a whole, the totality of economic phenomena . The term was first used by Ragnar Frisch on August 14, 1934. John Maynard Keynes is considered the founder of modern macroeconomic theory, after he published his book The General Theory of Employment, Interest and Money in 1936 (eng. The General...

The paradox of value (paradox of water and diamonds, or Smith's paradox). Adam Smith is credited with formulating the paradox. Its essence: why, despite the fact that water is much more useful for a person than diamonds, the price of diamonds is much higher than the price of water?

Economics (from other Greek οἰκονομία, literally - “the art of housekeeping”) is a set of social sciences that study the production, distribution and consumption of goods and services. Economic reality is the object of economic sciences, which are divided into theoretical and applied.

Economic evaluation methods are widely used in program evaluation. Among the most well-known and often used in practice, cost-benefit analysis and cost-effectiveness analysis can be distinguished.

“Creative” or Creative accounting is a set of legal methods by which an accountant, using his professional knowledge, increases the attractiveness of financial statements for interested parties and reduces the tax burden for the company he works for.

Rational expectations theory (abbreviated as TPO) is a concept of macroeconomics, originally developed by John F. Muth in 1961 and developed by Robert Lucas in the mid-1970s (for which Lucas was awarded the Nobel Prize in Economics in 1995). economics), as well as Christopher Sims and Thomas Sargent (they were awarded the Nobel Prize in Economics "for their empirical study of cause and effect in macroeconomics").

The paradox of thrift is a paradox in economics described by American economists Waddil Ketchings and William Foster and studied, in particular, by John Maynard Keynes and Friedrich von Hayek.

Monetarism is a macroeconomic theory according to which the amount of money in circulation is the determining factor in the development of the economy. One of the main directions of neoclassical economic thought. Modern monetarism emerged in the 1950s as a series of empirical studies in the field of money circulation. The founder of monetarism is Milton Friedman, who later won the Nobel Prize in Economics in 1976. However, the name of the new economic theory was given by Karl ...

Conspicuous consumption (eng. conspicuous consumption, prestigious, ostentatious, status consumption) - wasteful spending on goods or services with the primary goal of demonstrating one's own wealth. From the point of view of the conspicuous consumer, such behavior serves as a means of achieving or maintaining a certain social status.

Reproduction is the constant renewal of the production process. It has several models: simple (constant), extended (increasing), narrowed (decreasing).

Prediction markets are a type of speculative markets; their purpose is to make predictions. In such markets, assets are created whose ultimate monetary value is tied to a certain event (for example, whether the next American president will be a Republican) or a parameter (for example, what sales will be in the next quarter). Thus, current market prices can be interpreted as a forecast of the probability of a certain event or parameter value. We can say that the markets ...

The broken window metaphor (sometimes translated as "the parable of the broken window") is a metaphor given by the economist Frédéric Bastiat in his essay Ce qu'on voit et ce qu'on ne voit pas ("On what is seen and what what is not visible"), 1850. According to Henry Hazlitt, this metaphor illustrates one of the common misconceptions about economics, namely that any disaster can contribute to economic development.